Every economy the whole world over is reeling from the pandemic’s impact.

But individual governments have responded differently according to their needs. In India, for example, rescue efforts have included rice and beans for the poor.

More developed economies have pumped in funds to lend to firms, pay workers wages, and provide urgent assistance to the most vulnerable in their societies. The total global bailout fund was recently estimated by financial consultants at Barron’s as being more than $10 trillion.

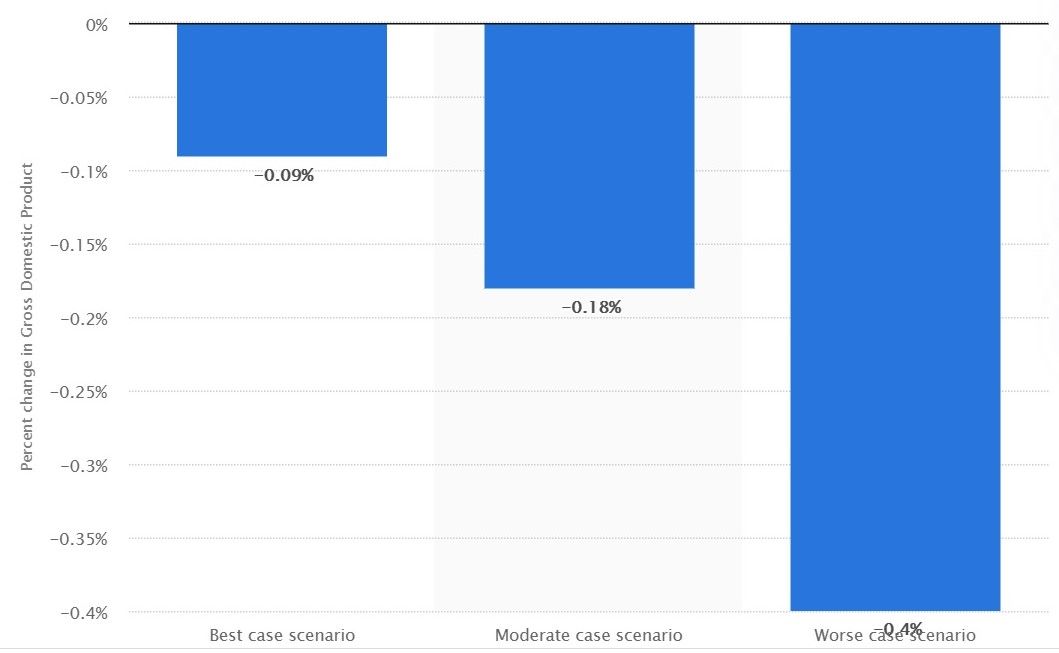

Despite this, economic forecasts are gloomy, with the Organization for Economic Cooperation and Development predicting the strongest warning on record that most major economies had entered a “sharp slowdown.” Meanwhile, Kristalina Georgieva, managing director of the International Monetary Fund (IMF) said, “We anticipate the worst economic fallout since the Great Depression.” And the World Trade Organization is forecasting double-digit economic declines for nearly every region in the world. The largest economic powers in North America and Asia being hit hardest.

But how are the major governments of the world reacting to the economic depression cause by COVID?

The United States of America

While the very latest unemployment figures surprised analysts with a blip of recovery, the scale of joblessness has been staggering. By mid-March one in six U.S. workers had filed for unemployment, some 30 million people.

In response, the Federal Reserve has acted quickly. The American-based think tank, the Council on Foreign Affairs reporting that, “… it will do anything within its power to support the economy and provide liquidity. Among the Fed’s historic actions have been: cutting interest rates close to zero, reducing bank reserve requirements to zero, rapidly purchasing nearly $2 trillion in Treasury bonds and mortgage-backed securities, buying corporate and municipal debt, and extending emergency credit to nonbanks.”

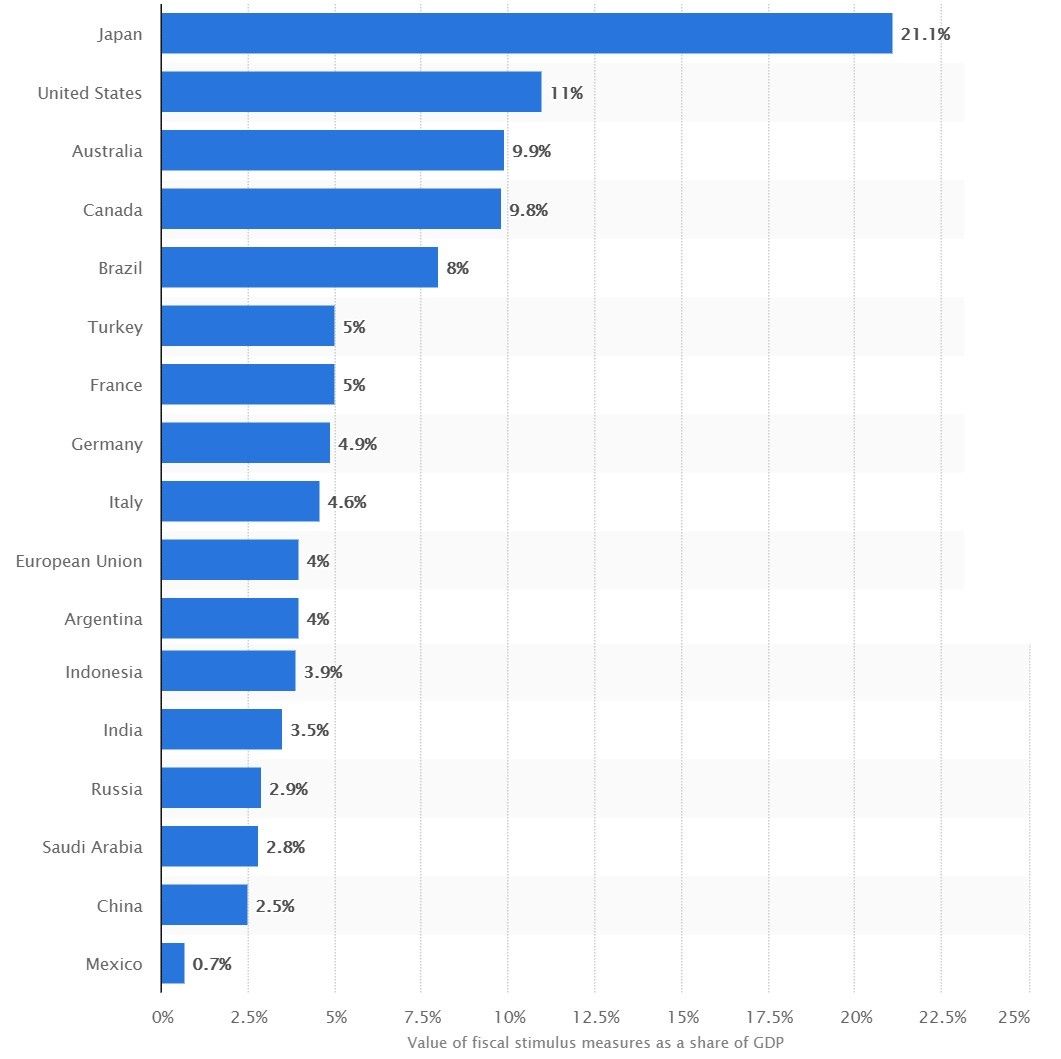

Meanwhile the government has passed bills granting $2.5 trillion of loans and grants to businesses, direct payments to individuals of up to $1,200, as well as further health care support for hospitals and care homes.

Germany

Like America, Germany has been quick and bold in its activity to support the economy, ignoring its normal policy of balancing government budgets.

As Chancellor Angela Merkel stated at the start of the lockdown, “We’re doing whatever is necessary, and we won’t be asking every day what it means for our deficit.”

Consequently, the country is spending €350 billion (about 10% of GDP) on loans, bailout grants, and even purchasing equity stakes in private businesses.

The UK

With the economy already on rocky ground as it prepared for the economic shudder of Brexit, the timing of the pandemic recession could not have been worse.

Despite this, the British government has pledged to spend as much as £400 billion (about 15% of GDP) in supporting individual parts of the economy.

China

China acted strongly following the 2009 financial crisis, investing $500 billion on a stimulus package to maintain economic growth.

Today, the Chinese economy is less stable and government debt has increased to 60% of GDP, so the Chinese central bank and politburo is less keen to spend its way out of the coronavirus economic slump.

Consequently, China’s response to the recession has so far been muted, cutting interest rates and a modest release of $80 billion in funds from the central bank to struggling businesses.

Central bank chief Yi Gang stating that, “The normal monetary policy should be kept as long as possible. The impact of the pandemic is temporary. China’s economy has strong resilience and great potential, while the fundamentals for high-quality development won’t change.”

Japan

Is predicting a drop in GDP of 3% in 2020, not only by the impact of coronavirus on domestic demand, but due to a fall in exports and the postponement of the Summer Olympics.

To combat the country’s worst recession since 2008, the government has begun pumping almost $1 trillion worth of aid and financial support into the economy, a sum equal to 20% of GDP.

The European Union.

EU finance ministers have already signed up to an aid package worth €500 billion, while Christine Lagarde, the European Central Bank’s president has pledged that there will be ‘no limits’ on the ECB’s defence of the eurozone economy. To date, the limit has been set at a €750 billion buy up of national bonds to support member states.

The Rest of the World

Most other major economies have reacted in similar fashion. Pouring in billions of dollars’ worth of aid and financial support.

In other parts of the world, international institutions have set forth their plans for aid packages to poorer countries. The Council on Foreign Relations describing how, “The IMF has set aside $100 billion to lend to member countries that are facing acute financial crises because of the coronavirus, with preference given to emerging economies. By early April, more than ninety countries had requested bailouts.” Adding that, “World Bank Group President, David Malpasssaid the bank was committing more than $150 billion to counter the pandemic’s effects. More than two dozen virus-related loan requests have been fast-tracked, with many more in the pipeline. Thus far, India has received the largest loan at $1 billion.”

The coronavirus impact on people has been catastrophic. But perhaps its biggest victim will be the global economy.

Only time will tell how deep and how long the upcoming recession will be.

Its length and depth will largely be dictated by the virus itself, how societies react to fresh waves of infection, and also how well government and international aid is spent.

Will it be enough? Watch this space.

Photo credit: Statista, Statista, Kaique Rocha from Pexels, Anna Shvets from Pexels, Gerd Altmann from Pixabay, & Gerd Altmann from Pixabay