The modern world needs rare earth elements. The trace minerals that perform the roles that other raw materials cannot.

As a result, a large number of industries, such as the consumer electronics, military hardware, high-efficiency generators in turbines and electric motors for wind power and other clean energy producers, permanent magnets production, modern ceramics, to name a few, are dependent on rare earth elements (REE).

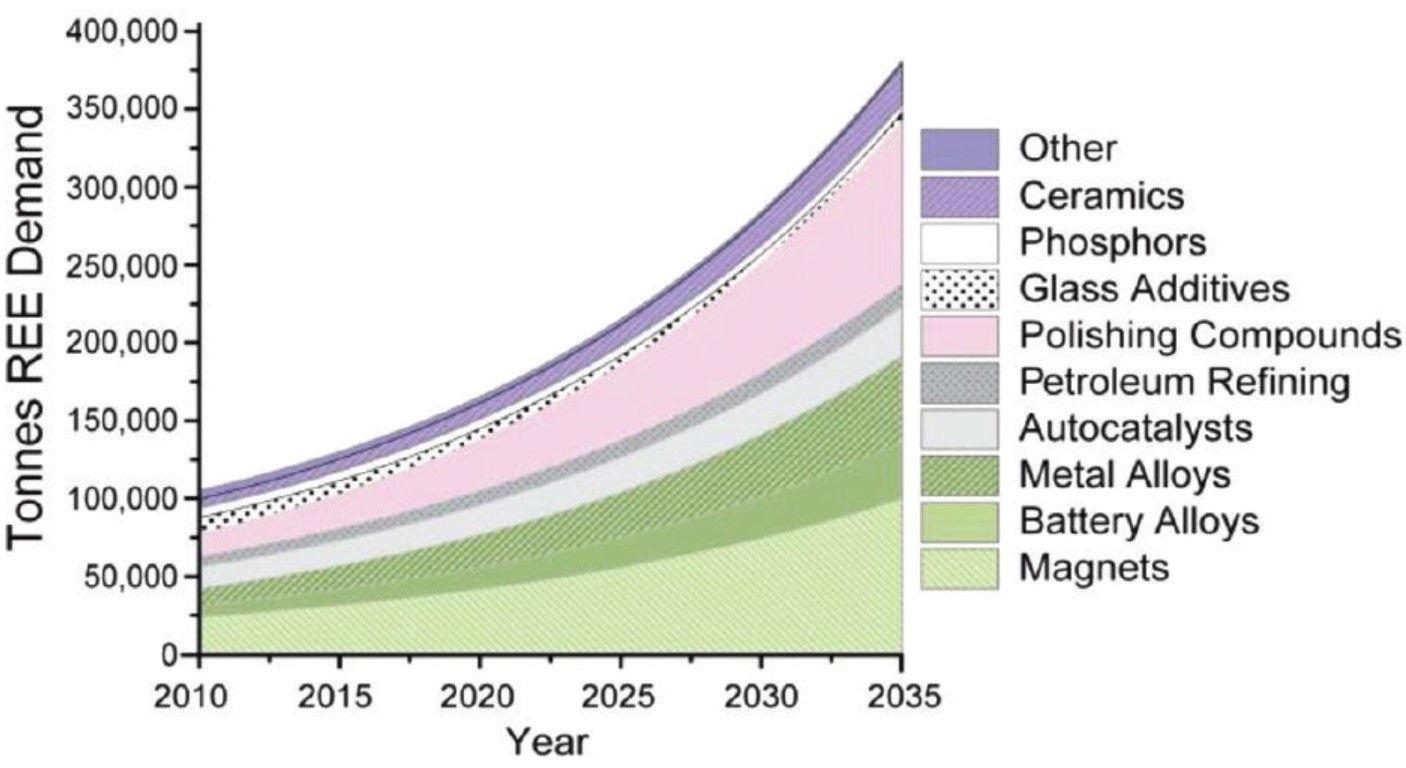

The good news is that a study on the issue by researchers from MIT concluded that, “There is currently no inequality between total REE supply and total REE demand.” However, it went on to state that, “Due to the many factors limiting growth in supply, there is no doubt that total REE supply will eventually lag behind total demand.”

This will naturally impact prices, with the report believing that, “A lack of REEs will cause large fluctuations in prices for many sectors of the global economy. In fact, the world is already paying for insufficient supply. For example, Dysprosium increased in price by almost 800% from 2006 to 2011.”

At first glance, finding out if there will be a long-term shortage of any given material seems easy; simple find out how much material there is in the Earth’s crust and divide by annual consumption to know when supplies will run out.

However, the issue is not so straight forward. Most rare earth elements are so trace, that knowing exactly how much is left is almost impossible to calculate. Additionally, many known sources are simply too difficult or too expensive to extract. For example, there are large reserves of manganese located in deep-sea noodles that can be found on the seabed. These sources are in small deposits with low concentrations and are very difficult to access. Extracting such sources is at present financially impractical.

Additionally, opening new mines is investment heavy, requiring government approval that, like any new mining project, can take years. This includes resolving environmental concerns, as ores containing REEs may also contain unwanted substances such as radioactive uranium and thorium which require specialised treatment and storage.

Furthermore, as well as paying for a new mine, investors must also build new refining capabilities, often in remote locations.

Finally, many REEs are not mined directly, but are instead only by-products of other processes. For example, hafnium is found in zirconium deposits, indium is sourced from zinc mining, and most gallium supplies are extracted from bauxite when alumina is refined.

For a better understanding of the issues of REE shortages, here we outline how the raw material indium is used, and the challenges faced to ensure that future supply meets future demand.

A History of Supplying Indium

Indium is a soft, silvery REE. When alloyed with tin and oxygen it forms a transparent, conductive oxide that is used to coat mobile, laptop, and TV screens. It is also used in the production of LEDs as well as infrared lasers for transmitting data down optical fibres. The world needs indium to operate the Internet.

Given the importance of indium, it would be easy to think that any supply shortage would be visible in price increases. However, as global production is as little as 800 tonnes per year, indium does not feature on many metal exchanges.

Additionally, single events can have catastrophic effects on price. As the journal PhysicsWorld reports, “Between 2002 and 2005, the price of indium rocketed from $100 per tonne to around 10 times that figure due to the closure of a major French refinery coupled with rising demand. More recently, indium’s price fell from around $500 per tonne to $300 per tonne after the Fanya Metal Exchange, a trading platform backed by the Chinese government, collapsed in 2015 amid allegations of large-scale fraud.”

The collapse of the Fanya exchange was significant because it officially reported 3,600 tonnes of indium in stock, with little evidence. As Max Frenzel, an expert on REE supplies at Germany’s Helmholtz-Zentrum Dresden-Rossendorf notes, for the figure to be accurate the exchange, “would have had to amass all the production in the whole of China for more than 10 years”.

Fortunately, since the Fanya collapse, demand for indium has steadied and combined production from China, South Korea, Canada, and Japan is satisfying markets.

The Future of Supplying Indium

Should demand grow in the future, markets can adjust by increasing the proportion of zinc smelters that produce indium, potentially doubling or tripling the supply rate of indium, although it, “typically takes between two and five years for a smelter to install new capacity”.

Alternatively, indium could be recycled. While extracting the trace elements on old and discarded screens is far from being economically viable, it is possible to improve efficiency or recycling during application. This is because more than 90% of indium alloy remains on the sputtering machine when the indium is being administered to screens.

In conclusion, Frenzel predicts that it will be 20 to 30 years before current supply chains will struggle to meet demand. And while this may allow many raw material suppliers to leave the sourcing challenges of indium to other generations, it is worth viewing indium as an example of the precarious nature of all REEs.

A mineral so vital to our digital world, yet so hard to extract, and even harder to recover once used.

To learn more about the challenges of REE supply, read: Examining the Supply Chain of Two Rare Earth Elements: Hafnium and Gallium.

Photo credit: MIT, Grimmmetals, Gokunming, Uknow, ACS, Geology, NYTimes, & Sonotek