Given that much of the petrochemical investment placed in America was to expand production to meet growing demand from China, the trade war stand-off is not good news for US chemical manufacturers. Houston-based, Westlake Chemical, blamed its 75% profit plunge in the first quarter of 2019 directly on ‘China depressed prices’ and ‘higher raw material costs’. While the ACC reports that chemical exports to China fell by 24% from last year.

This is the second and final part of Is a Bubble about to Burst in the Petrochemicals Industry? To read part one click here.

“We’ve come off a peak level of profitability,” said Mark Eramo, analyst and vice president of business development at IHS Markit. “It’s developing into a year that is going to be worse than we forecast.”

The problem for American chemical producers is even more acute, as the tariffs set up by the Trump Administration have been accused of damaging American businesses, as so many of them rely on raw materials that can only be sourced from China. This means that some non-American chemical manufacturers who do not have to pay tariffs are gaining a pricing advantage over U.S. firms.

“We’re buying those products, but then we are taking those inputs and turning them into American products, every single time. That’s what we do,” explains Robert Helminiak, vice president for legal and government relations at Socma, a trade group for specialty chemical makers.

As recently as July 2019, an article by Alexander Tullo, Senior Editor of Chemical & Engineering News (C&EN), the weekly newsmagazine of the American Chemical Society, explained how many American chemical manufacturers were being hurt, instead of protected, by the tariffs. He writes how, “Socma submitted a list of 269 chemicals and other materials that its members say would cause them hardship if hit with [further] tariffs. The Sun Chemical intermediates are on the Socma list. Itaconic acid, a dicarboxylic acid used to make an agricultural chemical that improves fertilizer uptake in plants, is also there. The Socma list also includes a slew of pharmaceutical products, including mannitol, used as a diuretic. A number of food ingredients made the Socma list as well, including vanillin and the emulsifier polysorbate 80.”

Petrochemical Exports

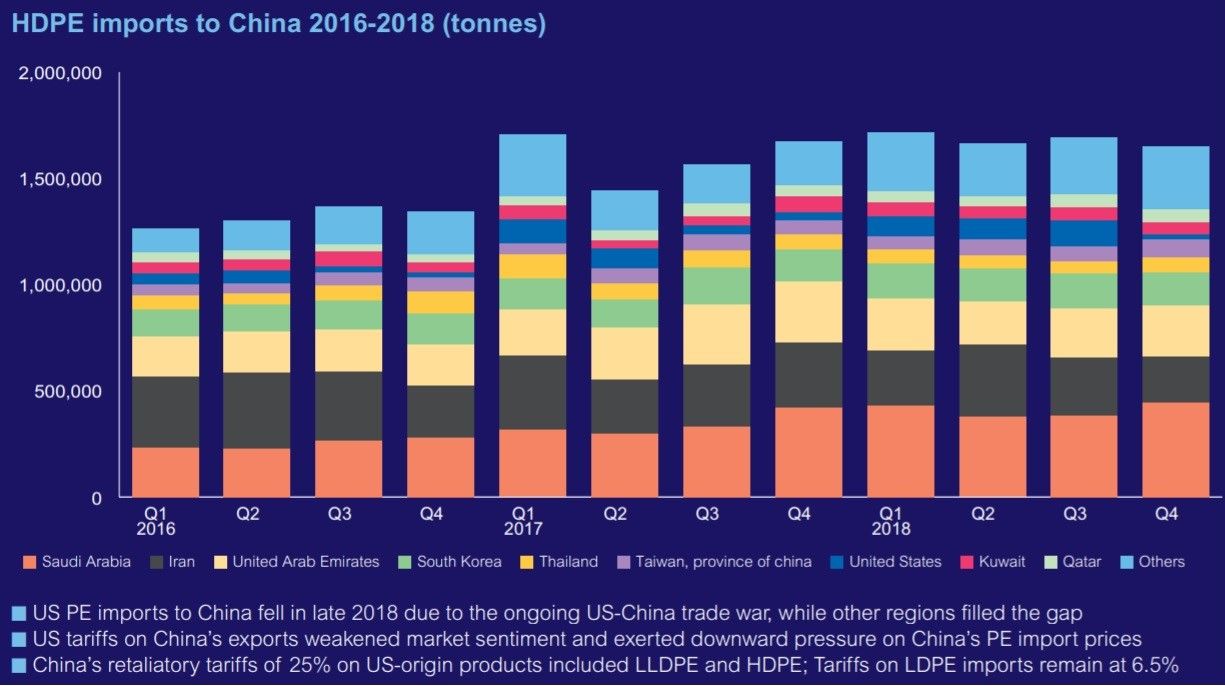

Additionally, many American petrochemical businesses are looking to other markets to make up for the restrictions in China. This has resulted in a global price drop, as US chemical producers attempt to enter already crowded European and Middle Eastern markets.

As Nick Vafiadis, a plastics analyst with the consultancy IHS Market, stated, “U.S. chemical companies are still making profits because of the low cost of natural gas needed to make their products, but they’re having to work much harder to sell into a more fragmented and competitive market.” With a recent ICIS report observing that prices for American high-density polyethylene purchased through long-term contracts have slid 13% percent since last year, while some Asian spot market prices for the same product were ‘down 23% percent in late June from just over a year ago’.

Petrochemical Demand

Adding to petrochemical industry woes are the long series of plastic bans and circular economy drives that continue to be a customer-relations nightmare for plastics producers and feedstock suppliers. As Deloitte analysts found, plastic bans and sustainability issues were mentioned as risks in SEC filings about 40% more often last year than in 2010.

While Paul Bjacek, chemical and energy research lead at Accenture, believes that eventually plastic bans and rising demand for recycled plastics could, in an extreme case, “… slash global demand growth for virgin petrochemicals in half by 2040, to 2 percent from about 4 percent per a year.”

Yet despite this, supply of chemicals for plastic products is about to reach an historic high, with ICIS reporting that, “In North America alone, the capacity to manufacture ethylene - a building block of most plastics - will have skyrocketed 73% by 2022 compared to the end of 2016.”

But while global demand for ethylene is expected to increase from 5 million to 6 million tons per a year, the current wave of ethylene projects going online is predicted to oversupply the market until 2030, forcing both prices and profits lower. Analysts at the research firm Wood Mackenzie, predicting that, “The worst of the glut is expected around 2023 to 2024”.

This is not to state that the petrochemicals industry will collapse, merely that there are tougher times ahead. Modern life requires plastics and petrochemical products, meaning that there will always be demand.

Furthermore, as standards of living go up in developing countries, so too will demand for petrochemical products. The International Energy Agency recently reported that developed economies use approximately 20 times more plastic per capita than developing nations. With India, China, and much of the Far East and Africa on the cusp of 20th century consumerist standards, the future is still rosy for the petrochemical industry as a whole.

As Andrew Slaughter, executive director of energy research at Deloitte, states, “The upside is that the chemical business is fundamentally healthy and growing faster than the fuel business, so long-term prospects are good.”

However, the industry needs to be aware that times have changed. Demand for sustainable chemical products will continue to grow, while tensions over oil supplies will constantly niggle at supply chains. Additional investment insecurity and the long-predicted global economic downturn also beckon to the end of an era.

As Robert Stier, senior lead of global petrochemicals at the research and pricing firm S&P Global Platts, makes clear, “The times of exceptional margins are over. The golden age is behind us.”

Photo credit: ICIS, Thoughco, Pepprlfuchs, Universityofwarwick,